Health & Fitness

Waiting for the "Bottom" to Buy a Home? Maybe You Shouldn't...

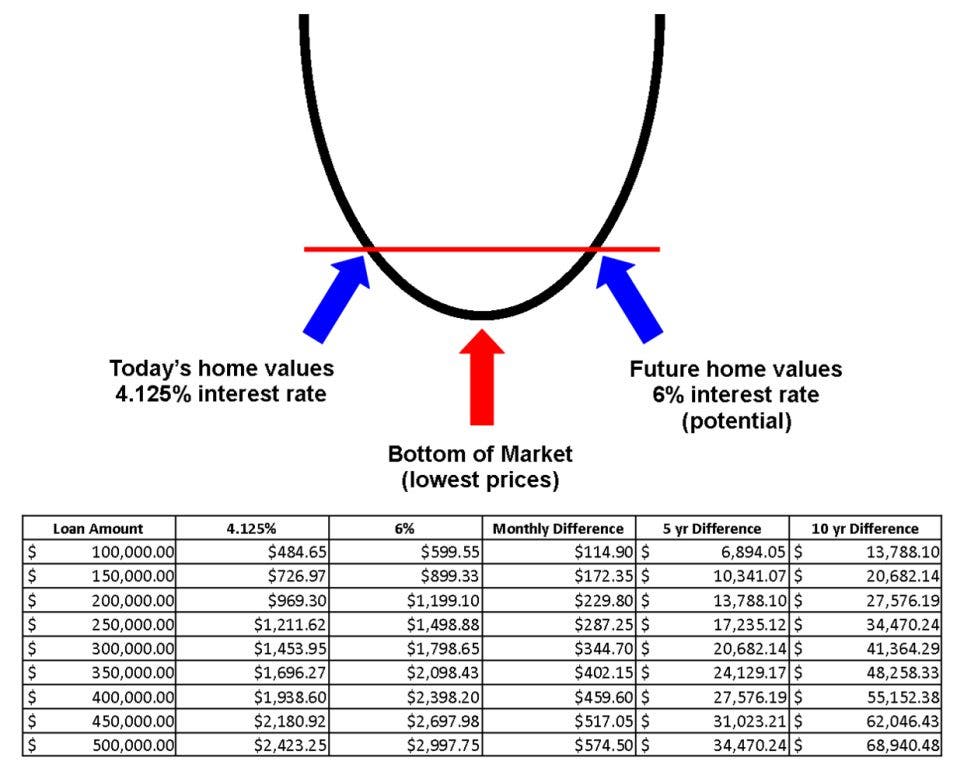

Whether you buy just after the bottom or just before the bottom, you'll be paying the same price, but you won't be getting the same interest rate.

When will we know we have hit the bottom of the housing market--that moment when prices are at their lowest? Not until we are beyond the bottom and can look back and recognize when prices bottomed out.

If you are "waiting for the bottom," you will most likely be buying just after the bottom. Whether you buy just after the bottom or just before the bottom, you'll be paying the same price, but... you won't be getting the same interest rate. That is why you shouldn't wait.

Today, my loan officer quoted me 4.125% on a 30 year fixed rate. Rates are going to go up sooner than later. The difference between a $300,000 mortgage at 4.125% and a $300,000 mortgage at 6% is $345 a month, which equates to over $20,000 in 5 years and over $41,000 in 10 years. Click on the accompanying chart to see how interest rates will affect mortgage amounts to help you decide if it truly is worth "waiting for the bottom."

Find out what's happening in Centrevillewith free, real-time updates from Patch.

I blog about real estate and life in Northern Virginia at MargieMac.com.